Following the European Central Bank (ECB) decision on 11 June, which included a 25 basis point adjustment, the European interest rate environment continues to evolve in a controlled and measured way.

Portuguese banks remain stable, well-capitalised, and actively lending. Competition between lenders continues to support attractive financing conditions for well-prepared borrowers, particularly international clients.

Portuguese banks remain stable, well-capitalised, and actively lending.

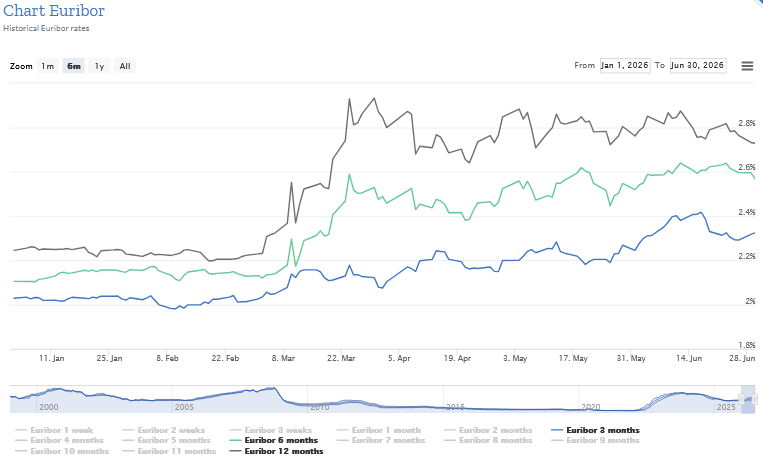

EURIBOR UPDATE – JUNE 2026

Current reference rates:

- 3M Euribor: 2.324%

- 6M Euribor: 2.568%

- 12M Euribor: 2.728%

While Euribor is an important reference, it is only one part of the final pricing. Lender appetite, structure, and borrower profile continue to have a significant impact on the outcome.

Sublime Insight: Euribor sets the direction, but the final conditions are shaped by how the case is structured and presented to the bank.

PORTUGUESE BANKS: ACTIVE BUT SELECTIVE

Portuguese banks continue to lend, but their approach is now more selective and structured.

Approval decisions are mainly driven by:

- Stable and verifiable income

- Debt-to-income capacity

- Liquidity and overall financial strength

- Quality and clarity of the application

Strong profiles continue to achieve very competitive results, but preparation now plays a key role.

Sublime Insight: Banks are still very open to lending, but they are increasingly focused on well-prepared, clearly structured applications.

WHY PORTUGAL REMAINS COMPETITIVE

Portugal continues to stand out as one of the most attractive mortgage markets in Europe.

Typical financing:

Residents

- Up to 90% financing depending on profile and property

Non-residents

- Typically 70%–80% depending on profile

Indicative pricing: - Variable: ~6M Euribor + 0.50%–0.70% for strong profiles

- Fixed: from ~2.25% depending on lender and client´s profile

International comparison:

- 🇵🇹 Portugal: ~2,25%-2,8%

- 🇬🇧 UK: ~4%–5%+

- 🇺🇸 US: ~6%+

Sublime Insight: Portugal remains attractive not only on price, but on balance: combining competitive rates with stability and consistent access for international buyers.

ACQUISITION OPPORTUNITIES: FINANCING AS A STRATEGIC CHOICE

For many international buyers, the decision goes beyond affordability, it is about how to structure capital efficiently.

Many of our clients could purchase a property in cash tomorrow if they wished.

The question is not: “Can I buy this property in cash?”

The question is: “Should I?”

If capital is already invested and generating 7%, 8% or even 10% returns, selling those investments to buy property outright may not always be the most efficient option.

Instead, many clients choose to structure financing in a more strategic way:

- Preserving invested capital

- Maintaining liquidity

- Keeping flexibility for future opportunities using leverage intelligently within a broader plan.

Sublime Insight: : The focus is no longer just ownership, it is making sure your capital continues to work while you invest in property.

2026 OUTLOOK

Looking ahead to 2026, the outlook remains positive.

Will the market become more demanding?

Probably.

Do I expect Portuguese banks to stop lending?

Absolutely not.

- We expect:

Continued strong competition between banks - Ongoing availability of financing for strong profiles

- Sustained demand for Portuguese real estate

- Growing importance of specialist structuring and advice

Portugal continues to offer one of the most attractive mortgage environments in Europe: the real advantage now lies in preparation, structure, and execution.